Rethinking Home Equity and Aging in Place

Lessons from the French Rente Viagère for the U.S. In-Home Care Industry

By

May 5, 2026

By: Aurelian Anghelusiu, Chief Relationship Officer at Care@Home4Life

Across the developed world, societies are confronting a profound demographic transformation. Populations are aging rapidly, longevity continues to extend, and the financial demands associated with retirement and long-term care are rising faster than most savings and pension systems were designed to sustain.

In the United States, millions of retirees face a paradoxical reality. Many possess significant wealth in residential real estate accumulated over decades of home ownership, yet lack the liquid income required to fund healthcare, support services, and long-term care during later stages of life. This phenomenon, commonly described as being “house-rich but cash-poor”, has become one of the defining challenges of modern retirement planning, and one of the largest unaddressed opportunities in the in-home care industry.

Americans now live longer than previous generations, often spending twenty to thirty years in retirement. Yet most retirement planning frameworks were designed for shorter time horizons, leaving a widening gap between longevity and financial preparedness. Nowhere is this gap more visible than in Florida and California, the two states that together house roughly one in four older Americans, and where in-home care agencies see firsthand how families struggle to align housing wealth with the daily cost of staying at home.

One of the most intriguing insights into how this challenge might be addressed comes not from recent financial innovation, but from a centuries-old real estate structure refined in France: the rente viagère. While the model itself is rarely used outside Europe, the principles behind it offer valuable lessons for how housing wealth can be turned into reliable income to fund aging in place.

The Longevity Economy and the Retirement Gap

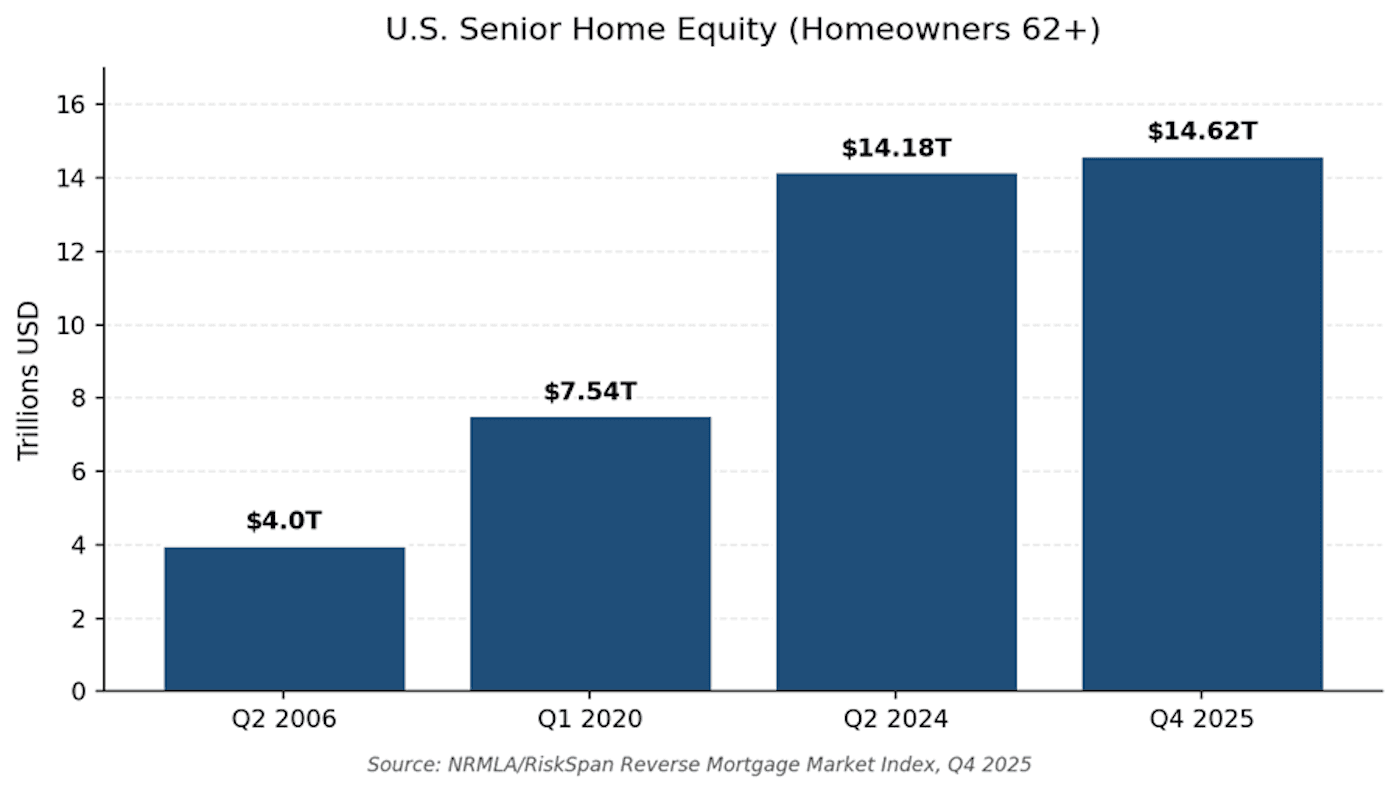

The scale of the issue becomes clear when examining the broader economic landscape. According to the NRMLA/RiskSpan Reverse Mortgage Market Index, U.S. homeowners aged 62 and older held approximately $14.62 trillion in home equity at the close of 2025, more than triple the figure recorded in 2006 and nearly double the level reached in early 2020. For most older households, residential property represents the single largest component of personal wealth.

Despite this concentration of assets, retirement income sources often remain limited. Social Security provides a critical foundation, but rarely covers the full range of housing, healthcare, and long-term care expenses. Private retirement savings, while helpful, can be depleted quickly when unexpected medical or caregiving costs arise.

AARP’s 2024 Home and Community Preferences Survey found that 75 percent of adults aged 50 and older want to remain in their current homes as long as possible, and 73 percent want to remain in their current communities. Yet 44 percent of the same group expect they may have to relocate at some point, primarily because of housing costs, the absence of accessible features, or the lack of in-home support. The desire to age in place is overwhelming; the financial infrastructure to make it possible is not.

The result, for in-home care agencies, is a market full of qualified, motivated clients who own their homes outright but feel they cannot afford the very services that would let them stay in them.

The Rising Cost of Long-Term Care

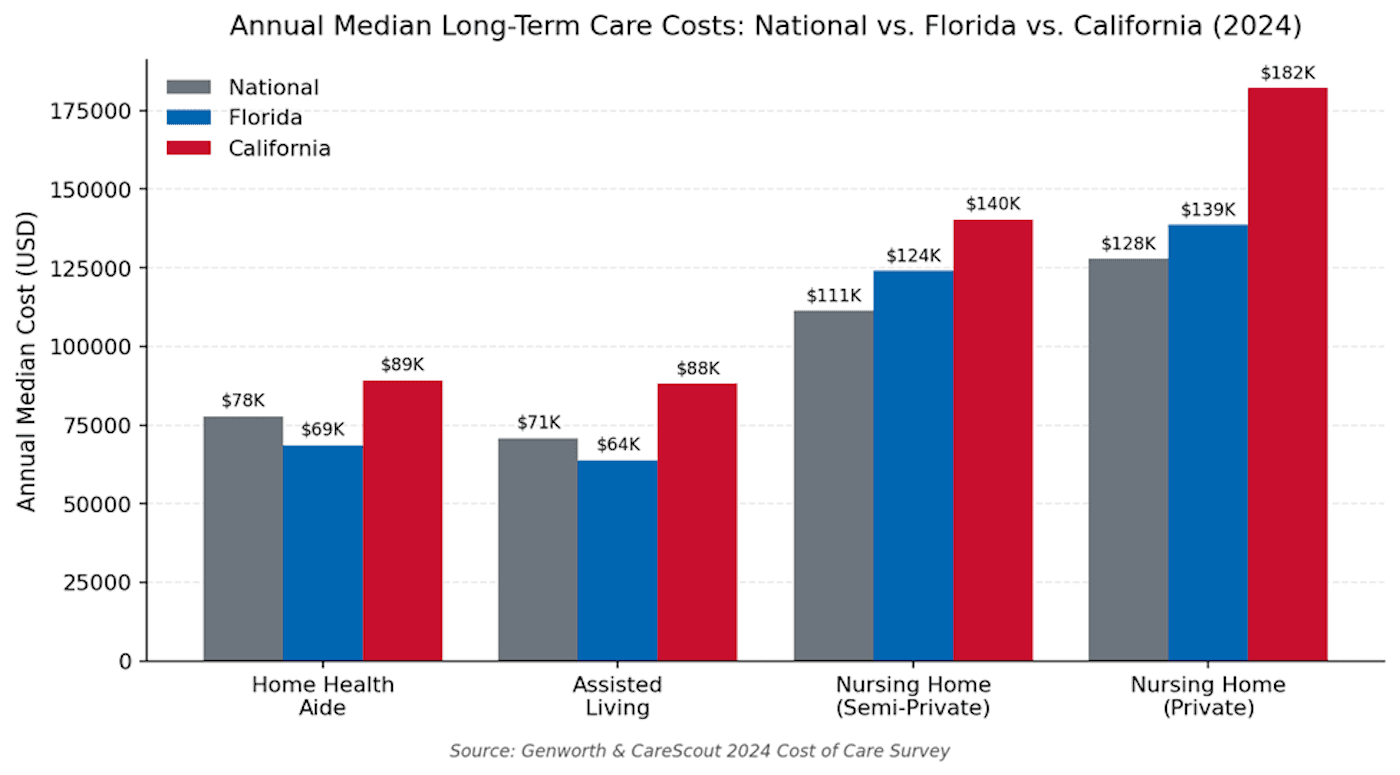

Long-term care costs are a major driver of this gap. The 2024 Genworth and CareScout survey shows that home health aide care averages nearly $78,000 annually, while assisted living exceeds $70,000. Nursing home care can surpass $127,000 per year.

These costs continue to rise faster than inflation, driven by labor shortages and operational expenses. For many families, the financial burden becomes unsustainable without accessing additional resources.

The Florida Picture: A Home-Rich State Built for Aging in Place

Florida highlights this challenge clearly. About 21 to 22 percent of residents are over 65, and many retirees own homes with significant equity, often from $300,000 and over $1,000,000.

This has created one of the largest populations of home-rich, mortgage-free older homeowners in the country. While the wealth exists, families often struggle with how to access it without selling the home.

Care costs add pressure. Annual median costs reach $68,640 for in home care, $63,885 for assisted living, and over $124,000 for nursing home care. Notably, two years of in home care can cost about the same as one year in a private nursing home, making home care a more appealing option.

State policies further shape decisions. Medicaid covers a large share of long term care but favors institutional settings, while other benefits offer limited support. As a result, using housing wealth to fund in home care is becoming one of the most practical paths for maintaining independence and dignity.

California: Higher Costs, Greater Equity

California presents a similar but amplified scenario. The state has one of the largest senior populations and some of the highest care costs in the country. Home health aide services exceed $89,000 annually, while private nursing home care can reach over $182,000.

At the same time, housing values are significantly higher. Many older homeowners hold properties worth over $1,000,000, often with low property taxes due to long-term ownership.

This creates an extreme version of the house-rich, cash-poor dynamic. High equity exists alongside limited income, making it difficult to fund care without disrupting living arrangements.

Policy changes, such as easing restrictions on accessory dwelling units, have helped support aging in place. However, financial alignment remains a challenge.

The French Rente Viagère Model

The rente viagère offers a different perspective. Originating centuries ago, it allows homeowners to exchange property value for a lifetime income stream while continuing to live in the home.

The structure typically includes an upfront payment and ongoing monthly income for life. It reflects a philosophy that treats the home as both a financial and personal asset.

Rather than forcing relocation or debt, the model supports continuity. It allows individuals to remain in familiar surroundings while accessing the value of their property.

Its longevity as a system highlights its adaptability and relevance, even in modern financial contexts.

Limitations of Traditional U.S. Solutions

In the United States, reverse mortgages are the most common tool for accessing home equity. While useful in some cases, they are fundamentally debt-based. Interest accumulates over time, reducing the remaining equity.

These products also operate independently from care planning. They provide liquidity but do not address long-term support or integration with healthcare needs.

This creates a gap. Financial tools exist, but they are not fully aligned with the realities of aging in place.

Emerging Models and Innovation

New approaches are beginning to bridge this gap by adapting concepts similar to the rente viagère. These models aim to integrate home equity, income generation, and care planning into a single framework.

By aligning these elements, they transform housing from a passive asset into an active resource. This shift allows homeowners to access funds while remaining in place and maintaining stability.

For example, a homeowner with significant equity but limited income could convert part of that equity into a predictable income stream. This income can then be used to fund in-home care services.

Organizations such as Care At Home For Life are helping families better understand these evolving solutions while delivering compassionate in home support. Readers can explore their services and community insights through their official platforms, including Instagram, Facebook, YouTube, and LinkedIn.

Implications for In-Home Care Providers

For in-home care agencies, this shift presents a significant opportunity. The challenge is not a lack of clients, but a lack of accessible funding.

Providers who understand how to connect housing wealth with care services can better serve this growing market. This includes:

• Addressing funding strategies during client discussions

• Building relationships with financial and legal professionals

• Educating families about available options

• Positioning services within a broader financial framework

By doing so, agencies move beyond service delivery and become partners in long-term planning.

Conclusion

The rente viagère demonstrates that home equity can serve a greater purpose than inheritance or passive wealth. When structured effectively, it becomes a tool for supporting independence, dignity, and financial security.

As the United States faces the realities of an aging population, new models that integrate housing, income, and care will become increasingly important. Florida and California are likely to lead this evolution due to their demographics and economic conditions.

For families, the opportunity lies in rethinking how existing assets can support present needs. For care providers, it lies in helping clients bridge the gap between wealth and accessibility.

The most valuable asset many retirees own is not just something to pass down. It is something that can support how they live today.